i-Scream Media: 93% of Korea’s Teachers, Four Times Earnings

A capital-light compounder hiding on the Korean micro-cap market — 31% margins, a return on capital most companies dream of, a near-10% dividend, and a balance sheet unlike any you’ve seen.

Every so often you find a business that makes you re-check the numbers, because they look too good for where the stock is sitting. iScream Media is one of them.

Almost every primary-school teacher in South Korea opens its software on their screen every day. It sells textbooks that schools re-order year after year. It keeps 31 of every 100 won of sales as operating profit, has grown that profit by roughly a quarter a year for three years, earns triple-digit returns on the capital it actually uses — and pays a dividend yielding close to 10%. And you can buy the whole thing for about four times last year’s earnings.

Ticker 461300 in Seoul. At ₩15,860 the entire company is worth about ₩200bn — and it’s sitting on roughly ₩182bn of cash and securities, about 91% of its own market value. Strip that out and the market is pricing the actual operating business, which earns ₩62bn of operating profit a year, at only around ₩8bn — a few million dollars. On paper, that’s not a valuation; it’s a rounding error. So the obvious question is: what’s wrong with it? The answer isn’t the business — it’s excellent. It’s what the owners do with the cash. Let’s take both apart.

What the company actually does

The heart of iScream Media is a piece of software called iScream S — the daily toolkit a Korean elementary teacher uses to run their classroom: lesson slides, worksheets, videos, quizzes, a library of more than 6.5 million teaching materials built over twenty years. Teachers pay nothing for it. That’s the clever bit: it isn’t where the money is, it’s the front door.

Because about 93% of the country’s primary teachers already work inside this free tool every day, iScream has an enormous head start at the thing that does make money — textbooks. In 2022 it began publishing certified primary textbooks under Korea’s new curriculum and immediately won the highest adoption of the thirteen licensed publishers, around 40–58% on its maths, science and social-studies books.

Why is that such a good business? Four reasons, in plain terms:

The state pays, but teachers choose. Schools pick the publisher; the government funds it. iScream just has to win the teacher — and it already owns the teacher’s daily routine.

It repeats. A new class of pupils arrives every year, so schools re-order the same textbooks annually. Not a one-off sale — a recurring, predictable stream.

It’s sticky. Once a teacher has built a whole year around a textbook and its matching materials in iScream S, switching means relearning everything. Most don’t bother.

It’s almost impossible to copy. A rival would have to rebuild twenty years and 6.5 million pieces of content — then prise teachers off a platform they already open daily.

Put those together and you get a genuine moat — a durable edge a competitor can’t cheaply buy or copy. The loop is the moat: a free platform everyone uses, feeding a paid textbook business that recurs every year and is a pain to leave.

Two smaller businesses sit alongside. iScream Mall, an online shop for classroom supplies, owns 90%+ of education e-commerce and brings in about a quarter of revenue at healthy margins — though its profit has stopped growing. And teacher training, where iScream is the #1 private provider, is small (~6% of sales) and actually loses a little money right now as it expands into in-person courses. Neither moves the needle. The textbook engine is the story.

The numbers are genuinely good

Revenue and operating profit compounded at ~24% and ~26% a year — and margins rose while they did it.

Revenue climbed from ₩104bn to ₩196bn over three years, about 24% a year; operating profit grew even faster, ₩31bn to ₩62bn. The tell of a quality business is right there: the operating margin went up as the company grew, from 29% to 31.5%. Once the content library exists, each extra textbook costs almost nothing to make, so profit outruns sales.

And there’s one number that really seals it: how much profit iScream squeezes out of the capital it uses. On the standard measure most stock screeners use — which counts the giant cash pile as “capital” — its return on capital is around 30%, already excellent. But that understates it badly. The operating business barely needs any capital to run, so the return on the money genuinely tied up in it is far higher — well over 50%, and north of 100% on a strict reading. In plain English: it makes a lot of money from very little. That is the single clearest fingerprint of a high-quality business — and it’s exactly what you’re not being asked to pay for.

(One caveat: reported net profit is bumpier than operating profit, because the company runs an investment portfolio whose swings flow straight through the bottom line. For the clean read on the business, watch operating profit.)

It quietly became a textbook company

Publishing went from half the business to two-thirds — and is now essentially all of the growth.

Three years ago revenue was split fairly evenly between textbooks and the shop. Today publishing is two-thirds of the company and effectively all of the growth: more grades covered each year (3–6 now complete), rising adoption, and a textbook price that’s climbed from ₩8,755 in 2021 to ₩11,287 in 2025.

The upside is that publishing is the highest-margin, stickiest, best-protected leg. The trade-off is that iScream now leans on a regulated, government-funded revenue stream — so education policy can move the numbers, for better or worse.

Why you can’t judge this on one quarter

Textbooks ship only in Q2 and Q4, so Q1 and Q3 look tiny — and Q1 is a planned seasonal loss every year.

Look only at iScream’s first quarter and you’d think it was tiny or collapsing. It’s neither — it’s the calendar. Textbooks are delivered in just two quarters, Q2 and Q4, so Q1 and Q3 are small by design and the company runs a seasonal loss in Q1 every year. Normal, not a warning.

Q4 2025 alone did ₩102bn — over half the year. The latest quarter, Q1 2026, came in at ₩15.3bn, up ~15% on the year before, with the seasonal loss slightly smaller than a year earlier. Judge this company on full years, never on one quarter.

It turns profit into cash — with one lumpy year

Free cash flow hit ₩48bn (about 25% of sales) in FY2025; the 2024 dip was a one-off content build.

Free cash flow — the cash left after running and investing in the business — was ₩48bn in FY2025, about 25% of sales. That’s strong. The dip in 2024 wasn’t a problem; it was a deliberate ₩22bn+ splurge on building an AI textbook product. Once that normalised, cash flow snapped back. iScream’s “capex” is really content spending, and it comes in lumps: a heavy build year flatters nothing, a normal year converts beautifully. FY2025 was normal.

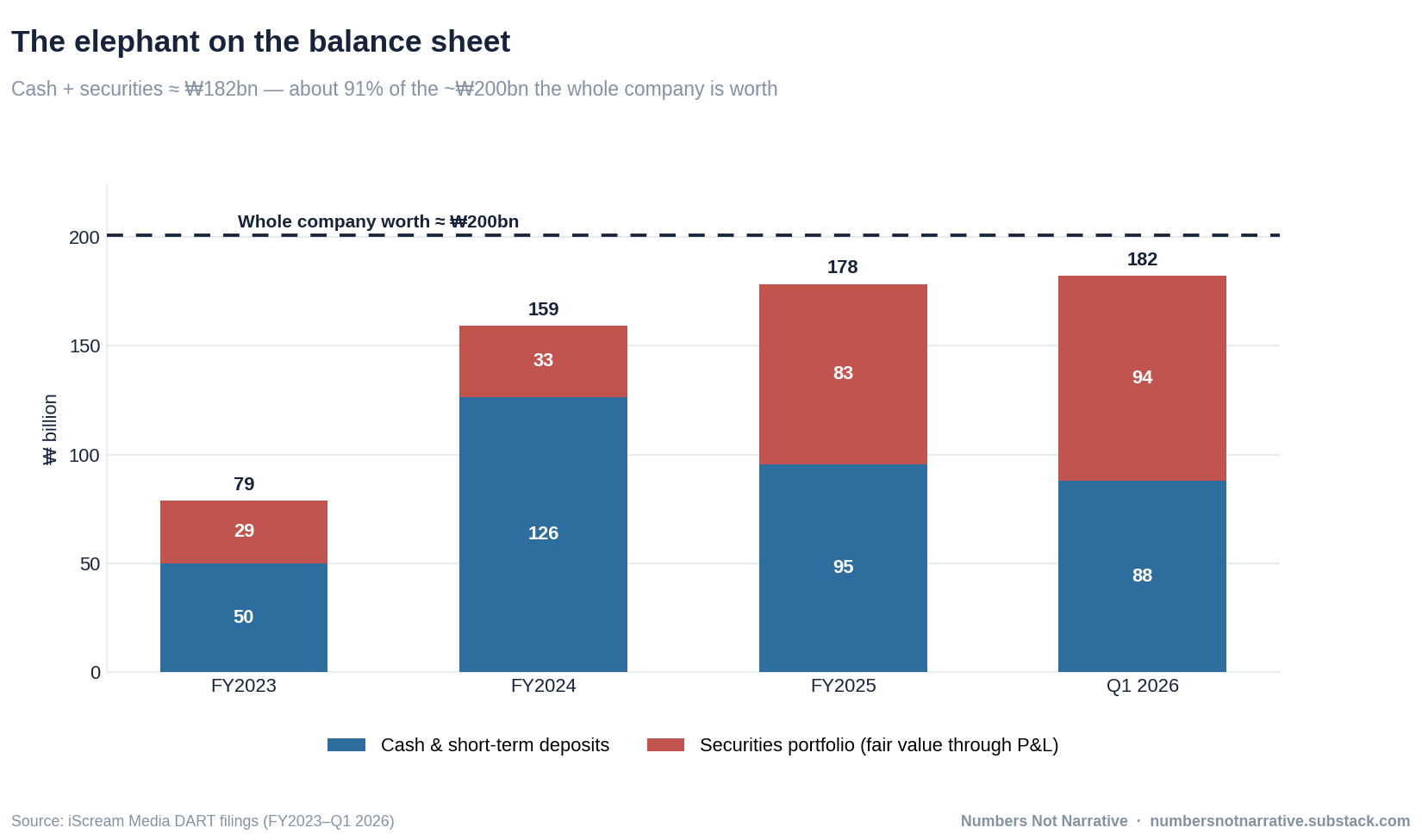

The elephant on the balance sheet

IPO cash was rotated into a securities portfolio worth ₩94bn — nearly as large as the entire operating business.

Now the part that complicates an otherwise easy story. The balance sheet is rock-solid — but look at what’s on it. iScream holds about ₩88bn of cash and ₩94bn of securities — together ₩182bn, roughly 91% of the whole ₩200bn company. The operating business that throws off all those lovely margins is a small slice of the assets; the rest is a war chest.

The trouble is that it isn’t clear that pile is really yours. It’s new, and it’s growing fast: the company raised money in its August 2024 listing and, instead of returning it or reinvesting it, poured it into an investment portfolio that has swelled from ₩33bn to ₩94bn in eighteen months. And some of those holdings are venture funds tied to the founding family — so a big slice of “your” cash is being run as an in-house fund, partly into related parties.

A note for the screener crowd. A typical data screener will show “cash & short-term investments” of about ₩111bn, not the ₩182bn here. The gap is that most of the securities (~₩70bn+) sit in long-term investments, which screens don’t count as cash. Read the actual filing and the pile — and the question hanging over it — is bigger than the screen lets on.

What happens next — a bigger runway than it looks

Here’s the pushback you’ll hear: Korea is running out of children. It’s true. The total school-age population is about 5.07 million today and is set to fall to roughly 4.25 million by 2029 — a ~3% annual decline — and the incoming first-grade cohort dropped below 300,000 for the first time in 2026. Fewer pupils eventually means fewer elementary textbooks.

But that misses how much room iScream still has to grow. It has grown straight through the demographic decline — publishing revenue rose 45% last year while pupil numbers fell — on three engines: it keeps winning share (40–58% adoption and climbing), it keeps raising prices (the per-book price is up ~29% in four years), and Korean families keep spending more per child (national private-education spend hit a record ₩29tn in 2024, up four years running).

And the bigger point: iScream is only just leaving its home turf. Management plans to take the publishing muscle it built in primary school and move, step by step, into the middle-school textbook market — a whole new set of grades and subjects to win. It’s pushing teacher training into secondary schools (where each teacher covers a single subject, so appetite for content is higher) and into the early-childhood and daycare market, and it’s taking its AI teaching tools abroad — to Vietnam, India and Japan. None of that is proven yet. But it means the addressable market is getting bigger, not smaller — and at this price you’re paying for none of it.

The catch — and why it’s shrinking

So why does a business this good trade this cheap? Two reasons, and both are real.

Control. The founding Park family owns roughly 61% of the company through its parent, SigongTech. That makes bankruptcy unthinkable — but it also means no outside investor can force that ₩180bn back to shareholders. Cash comes back only when the family chooses to send it.

Policy. iScream’s revenue rides on government decisions. The clearest reminder came in August 2025, when the government demoted the AI textbook iScream had spent heavily on from an official “textbook” to mere “educational material” — erasing the upside it had invested behind and forcing about ₩13bn of write-offs. When the state changes its mind, this business feels it.

But the catch is being actively chipped away. Under Korea’s national “Value-Up” programme, iScream now commits to paying out 40% of profit as dividends. The dividend more than doubled last year, to ₩1,554 a share — a yield of nearly 10% — and it uses only about 40% of free cash flow, so it’s well covered with room to grow. Add buybacks and total cash returned already tops 10% of the market value a year. The cash has started moving toward shareholders. The only question is how far it goes.

Putting a price on it

Price: ₩15,860

Market value (ex-treasury): ~₩200bn (~$150m)

Price-to-earnings (FY2025): ~4.1×

Price-to-book: ~1.0×

Return on capital (reported / operating): ~30% / >50%

Dividend yield: ~9.8%

Total shareholder yield (dividends + buybacks): >10%

Enterprise value: ~₩8bn — a few $m

FY2025 revenue growth: +29%

Operating margin: 31.5%

Free cash flow / sales: ~25%

Cash + securities: ~₩182bn (≈91% of market value)

Founding family control: ~61%

For the record, 13,302,433 shares are in issue, of which 598,969 sit in treasury (pledged against a convertible bond), so the free-float market value is about ₩200bn.

The summary is almost too simple: four times earnings for a business growing ~25% a year at 31% margins, with a near-10% dividend while you wait — and the ₩62bn-a-year operating company effectively thrown in for an enterprise value of barely ₩8bn. Numbers like that usually mean a business is dying. This one is thriving.

The verdict

iScream Media is two things at once. Underneath is a wonderful business — capital-light, high-return, sticky, growing, cash-generative, and rarely this cheap. Around it is the reason it stays cheap: an owner who controls the company outright, a revenue base exposed to the government’s pen, and a demographic tide that will eventually turn.

So the cheapness isn’t a mistake — it’s the price of the catch. Whether it’s a genuine bargain turns on one question: does the cash ever really reach outside shareholders? The Value-Up dividend already says “some, yes,” and broader Korean governance reform is a slow but real tailwind. If the cash starts flowing, the re-rating could be violent. If it doesn’t, you’re still collecting a near-10% yield on an excellent business you don’t quite control — far from the worst place to sit.

Numbers, not narrative: the business is as good as the headline figures suggest, and the stock is as cheap as it looks. The only real question is who the cash belongs to.

Not investment advice. The author may hold positions in the securities mentioned. Figures are from iScream Media’s DART filings (FY2022–Q1 2026), Statistics Korea and Ministry of Education data, and market prices as of 11 July 2026.

Hi, the company's disclosures seem to be in Korean, do you use AI translation to understand the disclosures/financials? Thanks.

Jakub, thanks for highlighting i-Scream Media CO., LTD. (461300 KS).

Looks interesting.

Why do they need to IPO?

The company had so much cash even before IPO.

Thanks