Dongsung FineTec (033500): the market is pricing peak. The order book says otherwise.

A ~₩550bn cryogenic-insulation maker trading at under 9× earnings, with a 25% ROE, net cash, and three years of revenue already signed. The bears have a real point — it’s just not the point the share

Value investors are trained to flinch at one setup in particular: the cyclical at the top of its cycle, throwing off record profits, wearing a single-digit P/E like a trap. Buy peak earnings at a multiple that only looks cheap until the denominator caves, and you lose money slowly. Dongsung FineTec looks like that company — and the stock, down ~46% from its ₩34,300 high to ₩18,460, is being priced like it.

I think the market has the right instinct and the wrong object. The cyclicality is real. But the thing that usually makes a peak-cycle short dangerous is sitting in the filings in plain sight: ₩2.08 trillion of order backlog, nearly three times last year’s revenue, for a product installed on a construction schedule the company neither controls nor can accelerate. You aren’t guessing at the next three years of revenue. You’re reading them off signed contracts.

Here’s the case from the numbers — then the reasons it might be wrong, because the red flags are not decorative.

The franchise: a toll booth at −163°C

Dongsung makes the insulation that holds liquefied natural gas at minus 163 degrees inside the cargo holds of LNG carriers. That’s the franchise. About 96% of revenue is one thing — polyurethane cryogenic insulation (reinforced foam, panels, membrane sheet) sold to shipyards. A small refrigerant-trading arm is the other 4%: a rounding error with some optionality bolted on.

This isn’t a commodity. The membrane containment systems (GTT’s Mark-III and NO96) are safety-critical on a thirty-year ship carrying a cryogenic, flammable cargo, so a supplier has to be qualified by the licensor and the yard — and nobody re-qualifies a vendor mid-programme to save a few percent. In Korea that’s produced a clean duopoly: Dongsung and Hankuk Carbon, with total global cold-insulation capacity under ~90 ships a year. Dongsung localised the technology first and runs ~34 ships of capacity, at roughly ₩25bn of content per large carrier.

So, plainly: Dongsung is a toll booth on the LNG construction bridge. Real barriers — qualification, switching costs, safety lock-in. No pricing power over its customers (three Korean shipbuilders that are its order book) or over GTT (which keeps the IP rent). Good economics while traffic is heavy; no leverage over whoever sets the toll. That tension is the entire bull-and-bear axis.

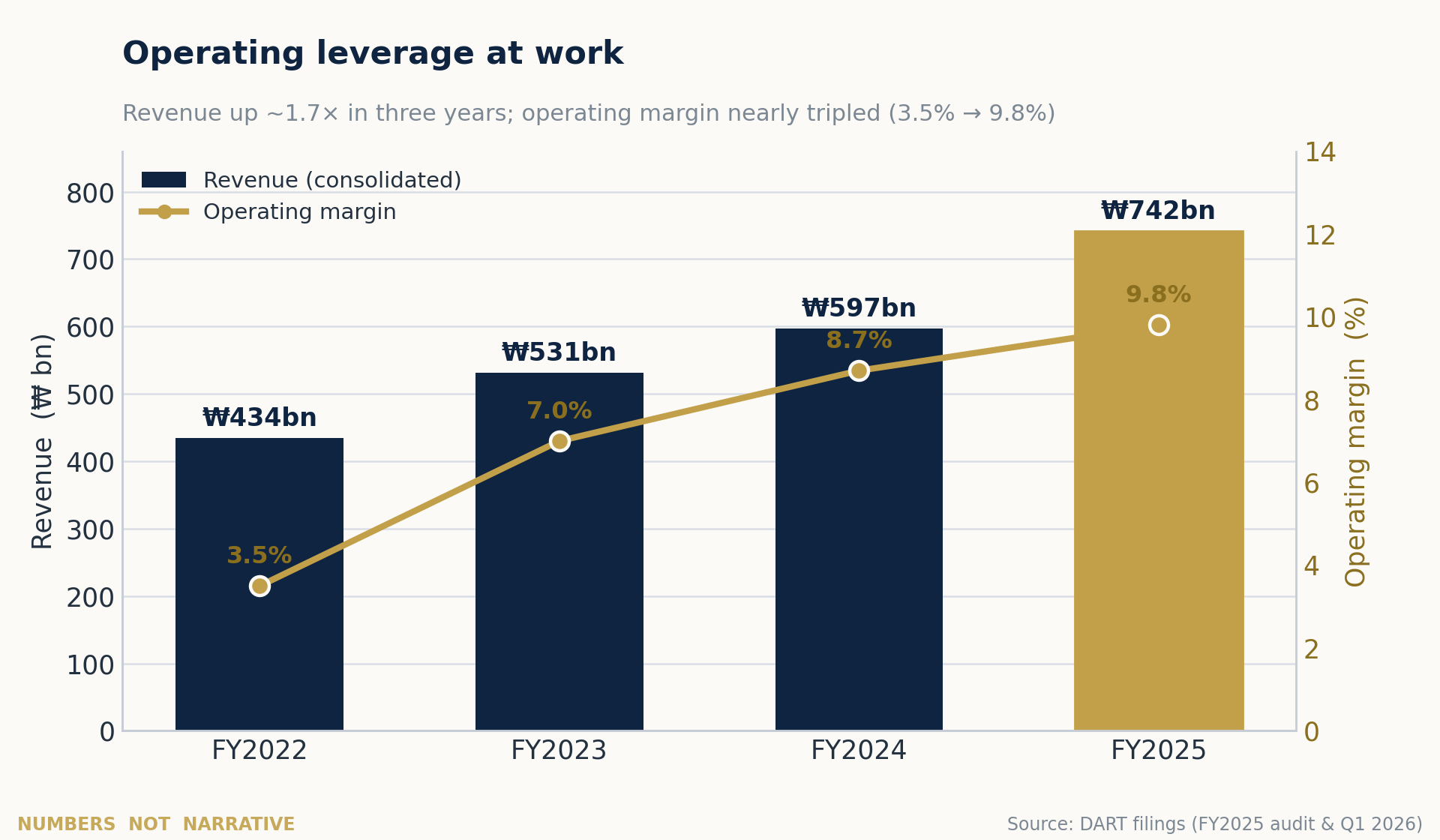

The operating leverage isn’t subtle

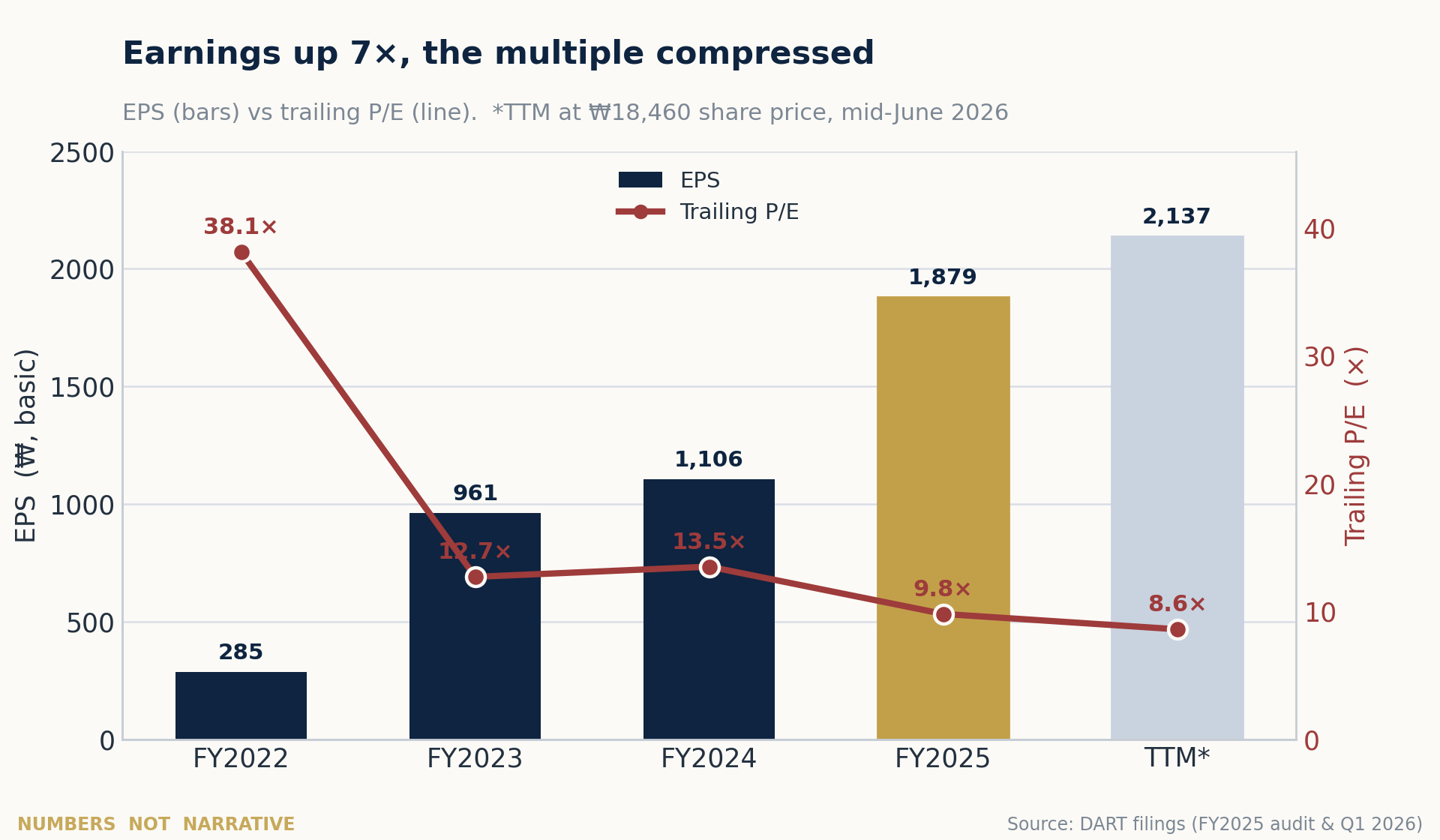

Three years ago this was a low-margin parts maker: ₩434bn of revenue, ₩8bn of profit. FY2025 closed at ₩742bn of revenue (+24%), ₩72.7bn of operating profit, and ₩56.2bn of net income (+43%) — roughly a 7× jump in earnings on a 1.7× rise in revenue, operating margin up from 3.5% to 9.8%, ROE through 25%. The latest quarter shows where that leverage comes from, in concentrated form.

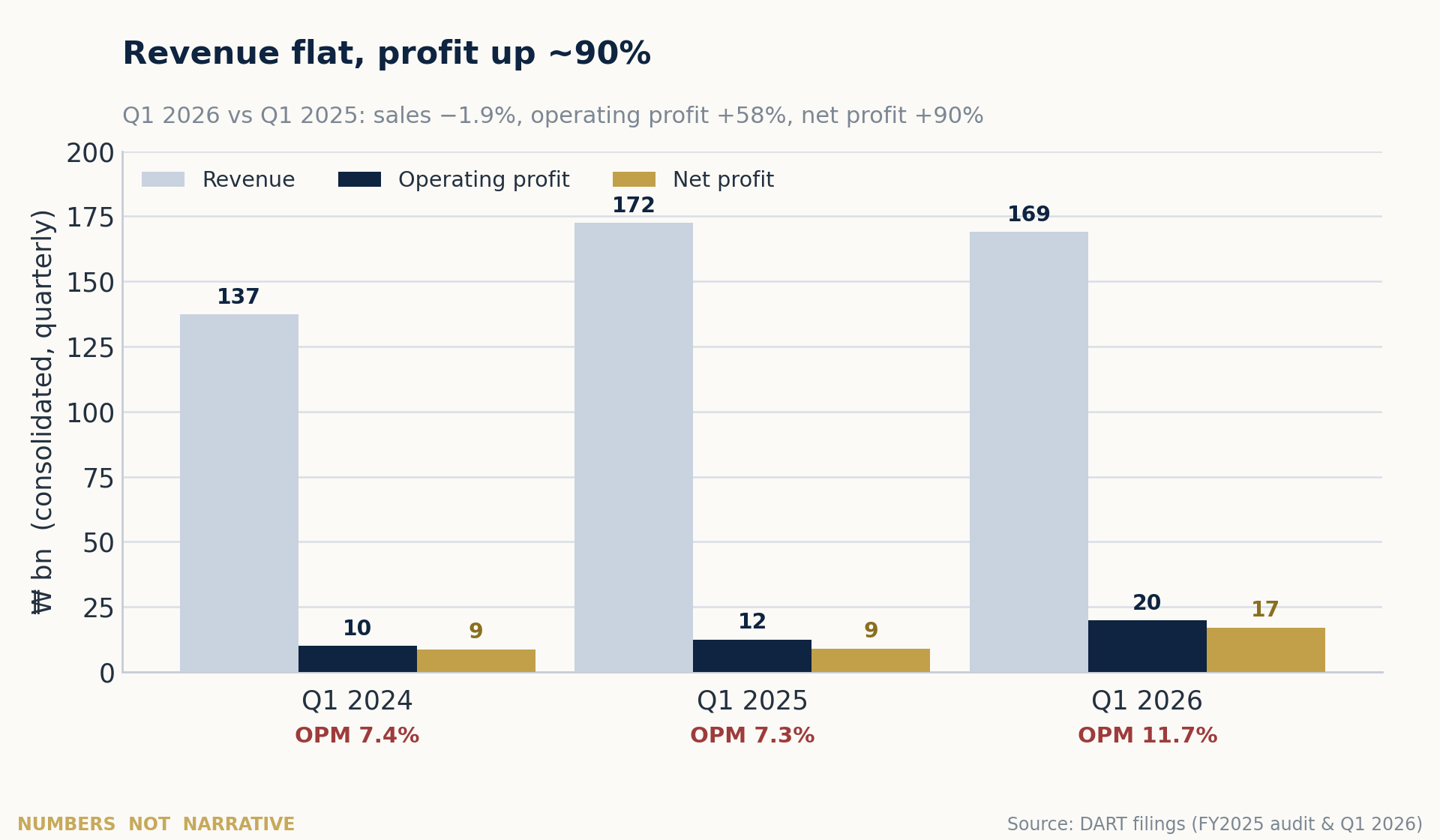

Q1 2026: a price story in a volume costume

Q1 revenue was ₩169bn — down 1.9% year on year. Yet gross margin went from 13.9% to 18.8%, operating profit rose 58%, and net profit rose 90% to ₩17.1bn. You don’t get that from working harder. You get it because what you sell is worth more and what you buy to make it costs less.

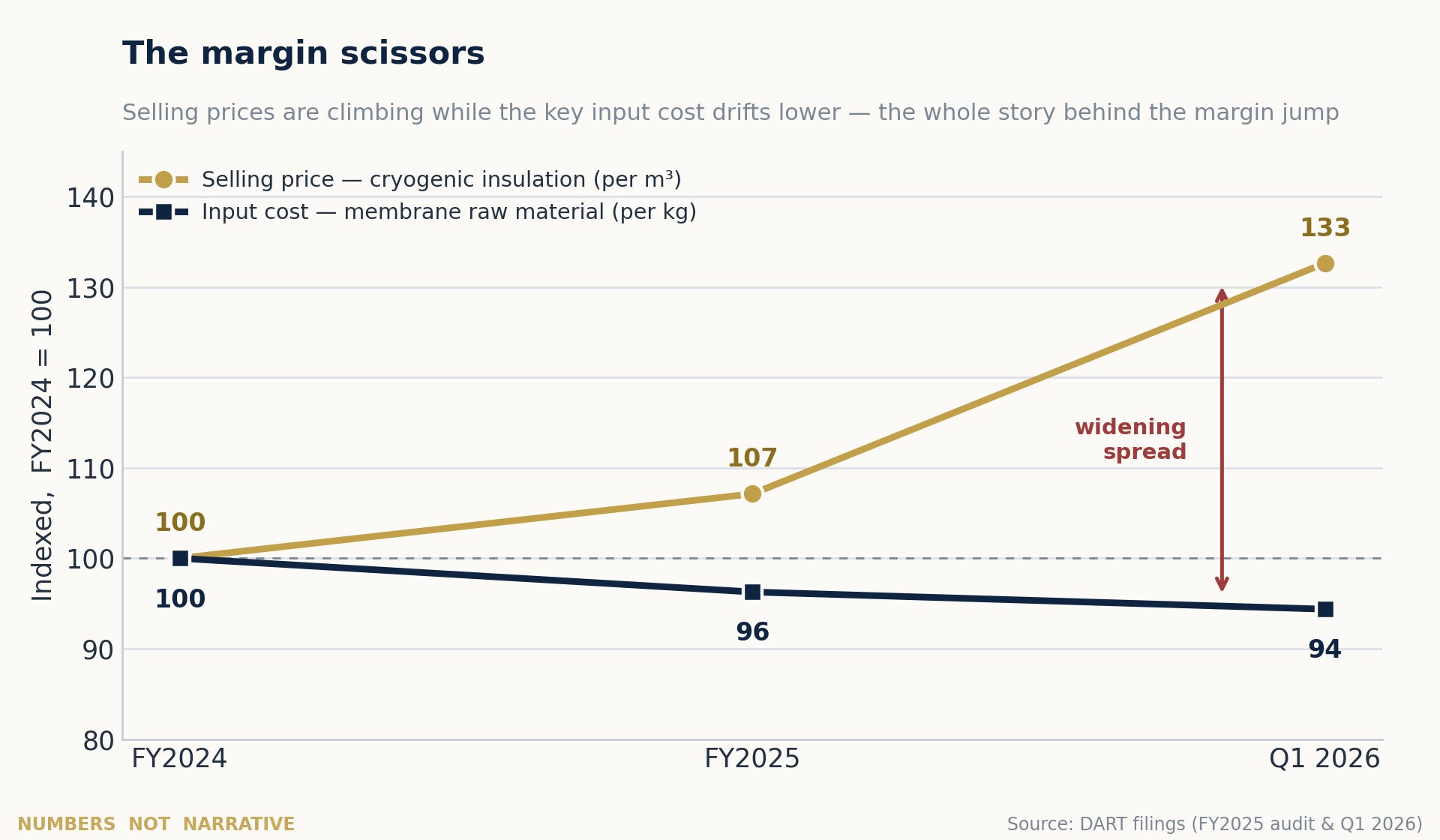

The filing’s price tables draw it cleanly. The average selling price of cryogenic insulation — quoted per cubic metre of carrier — went from ₩941,000 (FY2024) to ₩1,008,000 (FY2025) to ₩1,248,000 in Q1, up a third in fifteen months. Over the same window the per-kilo cost of membrane raw material fell, from ₩2,524 to ₩2,382. Prices up, costs down.

Two mechanics underneath, and they decide how durable this is. First, the revenue lag is a feature: insulation is fitted late in the build, so Dongsung books revenue three to four quarters after a yard cuts steel. The ships being insulated now were ordered in 2023–24, at higher prices than the 2021–22 vintage that once depressed margins — so the richest contracts are still flowing through, and management can see its own average selling price two years out. Second, the cost tailwind is luck, and should be treated as luck: ~60% of cost is raw material, mostly MDI and steel membrane; MDI sits near $2.1/kg versus the $4–6 of the Russia–Ukraine spike, helped by a weak won on dollar-priced sales. Both mean-revert. Underwrite ~9–10% normalised operating margins, not Q1’s 11.7%.

What’s already locked in

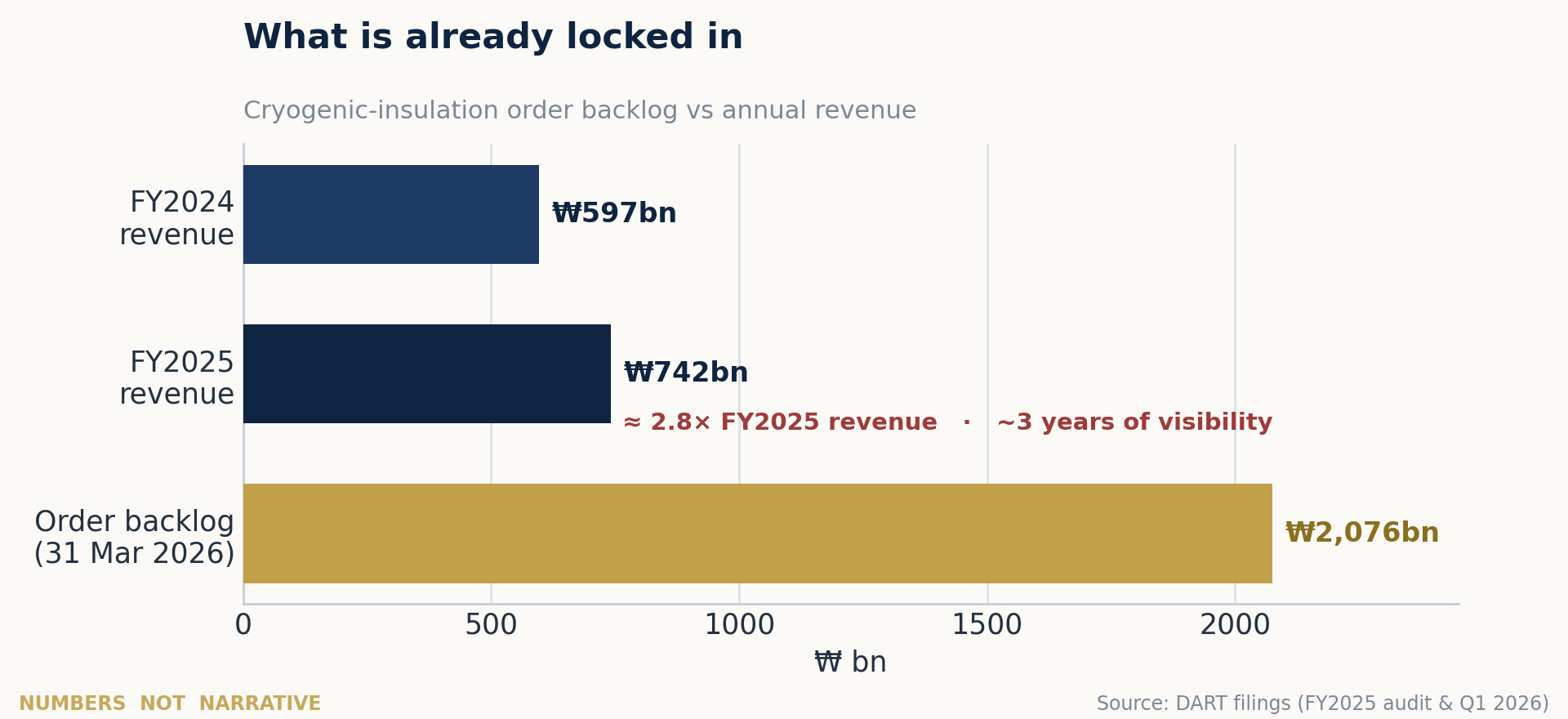

This is where Dongsung stops behaving like a normal cyclical. At 31 March the cryogenic-insulation backlog stood at ₩2,076bn — about 2.8× FY2025 revenue, three years of contracted work for HD Hyundai, Samsung Heavy, and Hanwha Ocean. The balance sheet agrees: inventory built to ₩178bn, and ₩112bn of customer advances sit in current liabilities against that book.

And the macro filling it from here isn’t a hope. The global LNG-carrier orderbook is at a record ~400+ ships, near half the fleet; Korean yards hold 70–75%, and deliveries peak in 2026–2028 — exactly Dongsung’s window, because it gets paid when ships are built, not ordered. New ordering did pause in 2025 (~16 carriers in eleven months) — the cliff the bears point at — but a record ~84 MTPA of US LNG capacity passed final investment decision in 2025, Qatar’s fleet renewal is live, and brokers model ~100–115 fresh orders in 2026 as 2028–29 slots open. Those refill the years after the current backlog.

The valuation: earnings up, multiple down

At ₩18,460, the market cap is ~₩554bn on 30.0m shares. Against that:

~8.6× trailing earnings, on ~₩2,140 of last-twelve-month EPS (about 10× on FY2025’s reported ₩1,879).

P/B ~2.1× on a 25% ROE — a touch over two times book for a business earning a quarter on it.

Net cash ~₩90bn — ~₩79bn cash plus ~₩11bn of short-term instruments against zero bank debt (the ₩7bn of short-term borrowings was repaid in the quarter). Strip it out and EV is ~₩460bn, putting EV/EBIT near 6×.

A ~1.8% dividend on a modest ~25% payout — room to grow, not a thesis.

Now set that against the company’s own history: 12–13× through 2023–24, north of 18× at the last peak, a trough-cycle average around 16–17×. It trades below its own cyclical floor while earnings still rise and three years of revenue are contracted. The de-rating has run ahead of any deterioration in the actual numbers. That gap is the opportunity.

Now the part that could cost you money

A cheap multiple on a peak cyclical is a trap until proven otherwise. The bear case, as strongly as I can put it:

One product, one cycle. ~96% of revenue is LNG-carrier insulation; there’s no second leg. The backlog that looks like a fortress empties on a schedule, and the real question isn’t 2026–28 earnings (largely locked) but normalised earnings power after it delivers — which depends on the 2026–27 ordering wave actually arriving.

Price-taker to three customers. HD Hyundai, Samsung Heavy, and Hanwha Ocean are the order book, they dwarf Dongsung, and they granted no price increases in 2021–22. Today’s pricing is a tight market, not structural leverage.

GTT keeps the crown jewels. Dongsung is a qualified manufacturer, not the IP owner — which caps how much of the chain it can ever capture.

China is the long shadow. Chinese yards are taking LNG share and don’t buy Korean insulation; Korea’s 2025 share recovery owed more to US port-fee actions stalling Chinese orders than to any moat of Dongsung’s.

The balance sheet flatters both ways. That ₩90bn of net cash is partly the flip side of ₩112bn in customer advances; as the book delivers and isn’t fully replaced, advances unwind and the cash normalises down. And the parent, Dongsung Chemical, owns ~39% — capital allocation will be made with its interests in view.

The optionality on the other side — DNV approval-in-principle for ammonia-fuelled tanks, liquid-hydrogen storage patents, refrigerant recycling into Korea’s 2027 mandate, a possible Alaska LNG tailwind — is real and free in the price, but immaterial today. Buy this for the LNG cycle and the balance sheet; treat the rest as a call option you didn’t pay for.

The verdict

Strip it to the frame. A niche manufacturer with a narrow-but-real moat, 25% ROE, no net debt, and three years of contracted revenue — at under 9× earnings, below its own cyclical-trough multiple, because the market has decided the cycle is over. The bears say it is over and you’re buying flattered, single-product earnings from a price-taker. The bulls say the 2026–28 delivery peak and the next ordering wave stretch the runway far enough that today’s multiple re-rates as visibility proves out.

Both can be true in sequence — a couple of very good, largely banked years, then a genuine question mark. That makes Dongsung less a forever-holding than a mispriced cyclical with an unusually long fuse: the rare case where the order book lets you price the next three years instead of guessing them. Size it as a cyclical, demand your margin of safety against normalised — not peak — earnings, and decide now what you’ll do when the backlog stops growing. Because the day that headline first prints lower, the multiple will move long before the revenue does.

Numbers, not narrative. The numbers are good. The narrative — peak, over, done — is what the price is selling you. Whether it’s right is the only question that matters, and the backlog buys you three years to answer it.

Analysis for discussion, not investment advice — I’m not your financial adviser, and every figure here should be checked against the primary DART filings before you act. Do your own work.

Figures from Dongsung FineTec’s FY2025 audited statements (DART, 19 Mar 2026) and Q1 2026 report (DART, 14 May 2026); market data as of mid-June 2026.